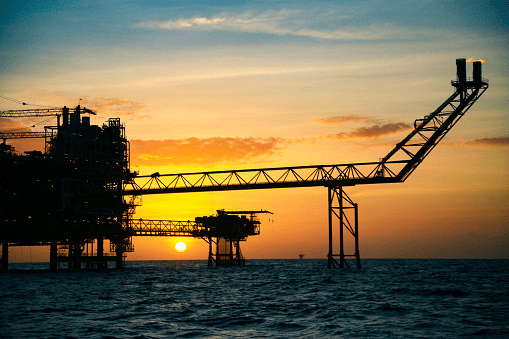

On Monday, oil prices surged as the West levied more sanctions on Russia, igniting fears of severe disruption to its oil exports.

Brent crude, the international oil benchmark, hiked 5.38% or 5.04 points to $99.16 per barrel. It slightly eased from a high of $105.07 in the early trade.

Similarly, the US West Texas Intermediate (WTI) crude soared 5.11% or 4.63 points to $96.28 per share. It gained as much as 7.00% to $98.00 per barrel earlier.

Last Thursday, both contracts went above $100.00 for the first time since 2014 as Russia escalated aggression towards Ukraine.

However, the initial spike pared after the White House’s first round of sanctions did not target Russia’s energy system.

Eventually, on Saturday, Western allies said they would disconnect specific Russian banks from SWIFT, a global payments system.

Russia is one of the leading oil and gas suppliers globally, especially in Europe. The country accounts for about 10.00% of the worldwide oil supply.

Experts explained that the latest sanctions do not directly target Russia’s energy industry but will trigger significant ripple effects.

Accordingly, the banking sanctions would make it highly difficult for Russian petroleum sales.

Then, Goldman Sachs bank increased its one-month Brent price forecast to $115.00 per barrel from the previous $95.00.

On Sunday, Russian President Vladimir Putin responded by putting its deterrence forces, which wield nuclear weapons, onto high alert.

Moscow’s invasion forces also had seized two small cities in southeastern Ukraine.

Meanwhile, today, Ukrainian and Russian officials arrived at the Ukraine-Belarus border for peace talks.

The meeting will focus on achieving an immediate ceasefire and the withdrawal of Russian forces.

Still, Ukrainian President Volodymyr Zelensky warned that the next 24 hours would be crucial for his country.

Oil Traders Focus on OPEC+ Meeting

The Organization of the Petroleum Exporting Countries (OPEC) and allies led by Russia, a grouping known as OPEC+, will meet on March 2.

Traders kept an eye close to the scheduled meeting to determine the group’s production policy for April.

They expected the oil alliance to stick to their plans of adding 400,000 barrels per day (bpd) of supply in April.

OPEC+ has kept oil supply in check as demand rebounded, catalyzed by concerns about Russia’s invasion.

However, the group lowered their forecast for the oil market surplus for 2022 by about 200,000 bpd to 1.10 million bpd. This decline underscored the current market tightness.

Furthermore, reports revealed that OPEC+ produced 972,000 bpd in January, way below their agreed targets.

COMMENTS